The Key to Unlocking the Potential of Options Trading

“Options have a language all of their own, and if you want to speak the language of options, you have to be able to understand the world of put-call parity.” – Lawrence G. McMillan

Put call parity is a fundamental principle in options trading that not only offers a deeper understanding of the market but also helps traders unlock countless opportunities. In this definitive guide, we’ll unravel the mystery of put-call parity, explore its implications, and reveal how to leverage its power to maximize profits and minimize risks. Are you ready to take the first step towards options trading mastery? Let’s dive in!

Table of Contents

- I. The Essence of Put Call Parity

- II. The Mathematical Formula Behind Put-Call Parity

- III. Factors Affecting Put-Call Parity

- IV. Arbitrage Opportunities and Put-Call Parity

- V. Practical Applications of Put-Call Parity in Trading

The Essence of Put-Call Parity

A Fundamental Principle in Options Trading

Put-call parity is a concept that explains the relationship between the prices of call and put options with the same strike price and expiration date. At its core, parity states that the value of a call option, combined with a cash amount equal to the present value of the option’s strike price, should be equal to the value of the corresponding put option plus the value of the underlying asset.

Put-call parity ensures that options are fairly priced and prevents arbitrage opportunities from arising. It is a critical concept that every options trader must understand to make informed decisions and accurately assess their trades’ potential risks and rewards.

The Mathematical Formula Behind Put-Call Parity

Cracking the Code of Options Pricing

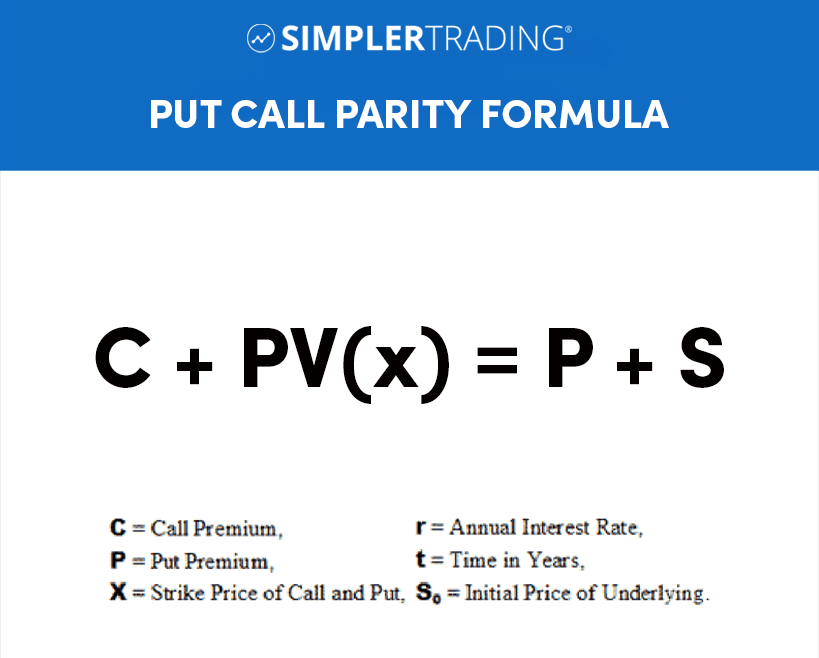

The formula for put-call parity is elegantly simple and can be expressed as: C + PV(K) = P + S

Where:

- C = price of the call option

- PV(K) = present value of the strike price (K), discounted at the risk-free interest rate

- P = price of the put option

- S = current price of the underlying asset

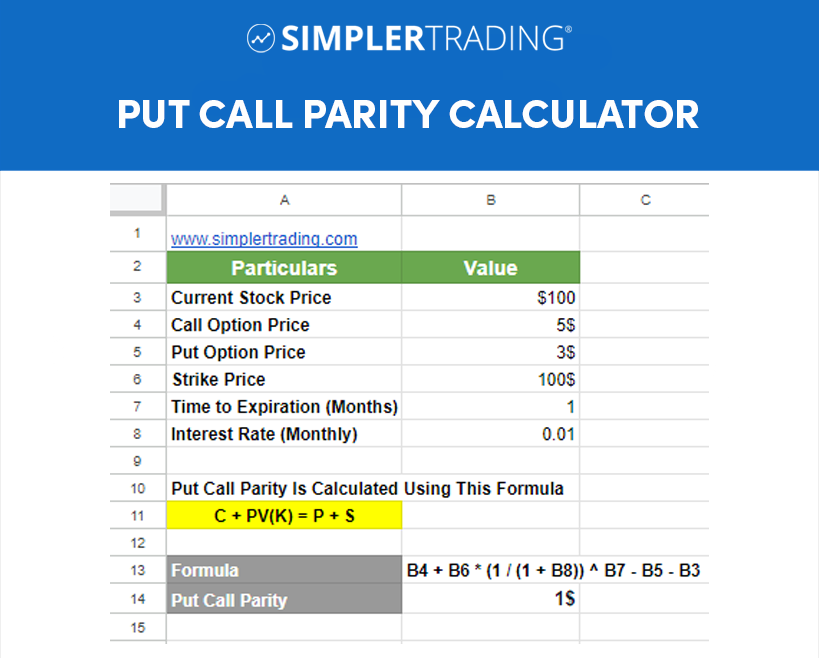

To understand this concept better, consider the following example. Suppose we have a stock trading at $100, a call option with a strike price of $100 expiring in one month, and a put option with the same strike price and expiration. The call option is priced at $5, and the put option is priced at $3.

According to put-call parity, the following relationship should hold: Call option value + Present value of strike price = Put option value + Underlying asset value

In this case, the equation would look like this: $5 + Present value of $100 = $3 + $100

Assuming an interest rate of 1% per month, the present value of the $100 strike price would be approximately $99.01. Therefore, the equation becomes: $5 + $99.01 = $3 + $100 or $104.01 = $103

This equation shows that the combination of a call option and a cash amount equal to the present value of the strike price should be equivalent to the combination of a put option and the underlying asset.

Understanding this formula is crucial for options traders, as it allows them to identify a potential mispricing in the market and make informed decisions about their trades.

Click here to and make a copy of a free Put/Call Parity Calculator seen in the image below.

Factors Affecting Put-Call Parity

Navigating the Variables That Drive Options Pricing

Several factors can impact the relationship between call and put options and understanding them is essential for mastering this concept. These factors include:

- Strike price: The predetermined price at which the option can be exercised. Changes in the strike price can affect the balance between call and put option prices.

- Time to expiration: The remaining time until the option’s expiration date. As time passes, the time value of both call and put options decreases, affecting the put-call parity relationship.

- Interest rates: Higher interest rates increase the present value of the strike price, which can affect the put-call parity equation.

- Dividends: The presence of dividends can also impact the relationship, as they affect the underlying asset’s value. Traders need to adjust the put-call parity equation to account for dividend payments.

By understanding how these factors influence parity, options traders can better assess their trades’ potential risks and rewards and make more informed decisions in the market.

Arbitrage Opportunities and Put-Call Parity

Exploiting Market Inefficiencies for Profit

When the put call parity equation is not balanced, it indicates that options are mispriced, creating potential arbitrage opportunities. Arbitrage is the practice of taking advantage of price differences in different markets to make risk-free profits. In the context of put-call parity, traders can exploit this mispricing by simultaneously buying and selling the corresponding call and put options, along with the underlying asset, to lock in a risk-free profit.

It’s important to note that arbitrage opportunities are often short-lived, as market participants quickly adjust prices to restore the put-call parity equilibrium. Therefore, traders must be vigilant and act quickly to capitalize on these opportunities when they arise.

Practical Applications of Put-Call Parity in Trading

Leveraging Put-Call Parity for Smarter Trading Decisions with Real-World Examples

Put-call parity has several practical applications in options trading that can help traders make smarter decisions:

Assessing option mispricing: By understanding put-call parity, traders can quickly identify mispriced options and exploit arbitrage opportunities or make better-informed trading decisions.

- Example: Suppose a stock is trading at $100, and a call option with a strike price of $100 and expiration in one month is priced at $5. The corresponding put option with the same strike and expiration is priced at $4. The risk-free interest rate is 1% per annum. Using the put-call parity equation, C + PV(K) = P + S, we can calculate the present value of the strike price (PV(K)) as $100 / (1 + 0.01)^1/12 = $99.92. The equation becomes $5 + $99.92 = $4 + $100, which simplifies to $104.92 ≠ $104. This indicates that the options are mispriced, and a trader can exploit this arbitrage opportunity by simultaneously buying the put, selling the call, and buying the stock to lock in a risk-free profit of $0.92 per share.

Evaluating potential trade setups: Put-call parity can help traders compare the potential risks and rewards of different options strategies, allowing them to select the most suitable approach for their trading objectives.

- Example: A trader is considering two strategies: a covered call or a protective put. By analyzing the put-call parity relationship, the trader can determine which strategy offers a better risk-reward profile based on the current market conditions, option prices, and risk tolerance.

Hedging existing positions: Put-call parity can be used to identify appropriate hedge ratios for existing options positions, helping traders protect their portfolios from adverse market movements.

- Example: A trader holds 100 shares of a stock trading at $50 and wants to hedge against a potential decline in the stock price. By utilizing the put-call parity equation, the trader can determine the appropriate number of put options to buy to create a protective hedge. If the trader identifies that one put option with a strike price of $50 and expiration in one month costs $2, they can use the put-call parity equation to calculate the corresponding call option price and determine the hedge ratio, ensuring that their portfolio is protected from potential downside risk.

By incorporating put-call parity into their trading toolbox, options traders can make more informed decisions, minimize risk, and maximize their potential for profit.

Key Takeaways

💡 Put-call parity is a fundamental principle in options trading that explains the relationship between call and put option prices.

💡 The put-call parity equation is C + PV(K) = P + S, where C is the call option price, PV(K) is the present value of the strike price, P is the put option price, and S is the underlying asset price.

💡 Factors affecting put-call parity include strike price, time to expiration, interest rates, and dividends.

💡 Put-call parity allows traders to identify mispriced options, evaluate potential trade setups, and hedge existing positions.

Conclusion

Put-call parity is a vital concept for options traders, providing valuable insights into market dynamics and helping traders make more informed decisions. By mastering put-call parity, you can unlock countless opportunities to maximize your profits and minimize your risks in the exciting world of options trading. If you have enjoyed learning about the put/call parity, consider joining the Simpler Trading Simpler Central Trading Room. For only $7 for 30 days, you will gain access to a wealth of knowledge from traders who have over 200 years of combined experience. The question you should be asking yourself is whether you can afford not to join…

Remember…

“Don’t try to buy at the bottom and sell at the top. It can’t be done except by liars.” – Bernard Baruch

FAQs

A: Put-call parity is a fundamental principle in options trading that states the relationship between the prices of call and put options with the same strike price and expiration date.

A: The put-call parity equation is C + PV(K) = P + S, where C is the call option price, PV(K) is the present value of the strike price, P is the put option price, and S is the underlying asset price.

A: Put-call parity helps traders identify mispriced options, assess potential trade setups, and hedge existing positions, allowing them to make more informed decisions and maximize profits while minimizing risks.

A: Factors affecting put-call parity include the strike price, time to expiration, interest rates, and dividends. These factors influence the value of the underlying asset and the prices of the call and put options.

A: Arbitrage opportunities arise when the put-call parity equation is not balanced, indicating that options are mispriced. Traders can exploit this mispricing by simultaneously buying and selling the corresponding call and put options, along with the underlying asset, to lock in a risk-free profit.

References

Hull, J. C. (2017). Options, Futures, and Other Derivatives (10th ed.). Pearson Education.

Investopedia. (2021). Put-Call Parity. Retrieved from https://www.investopedia.com/terms/p/put-callparity.asp

CBOE. (2021). Understanding Put-Call Parity. Retrieved from https://www.cboe.com/education/getting-started/quick-facts/put-call-parity