The Basics of Option Premium: What It Is and How It’s Calculated

Introduction

Option premium is a critical concept for any trader or investor to understand, as it plays a crucial role in the price of options contracts and the potential profitability of options trades. But for many beginners, the concept of option premium can be confusing and overwhelming. In this post, we’ll break down the basics of option premium and give you the tools you need to understand how it’s calculated, what factors influence it, and how it changes over time. By the end of this guide, you’ll have a strong foundation in the fundamental principles of option premium and be well on your way to becoming a more confident and successful options trader.

Table of Contents

I. Introduction

- Table of Contents

- The Condensed Version

- Definition of option premium

II. What is option premium?

- Explanation of option premium as the cost of an options contract

- How option premium is determined by various factors, including underlying stock price, strike price, expiration date, and implied volatility

III. How is option premium calculated?

- Explanation of the Black-Scholes model for calculating option premium

- Intrinsic Value As a Factor In Option Premium

- Extrinsic Value As a Factor In Option Premium

IV. How does option premium change over time?

- Explanation of time decay and how it affects the option premium

- The relationship between the option premium and implied volatility

- How events such as earnings announcements or changes in market conditions can impact option premium

- Volatility Crush

V. Conclusion

The Condensed Version

Want the short version? Here’s a condensed version of the entire blog post. To gain a thorough understanding, please consider reading each section carefully to fully benefit from the information that we carefully researched for you.

- Options premium is the cost of an options contract

- Options premium is determined by various factors including the current market price of the underlying asset, the strike price, the expiration date, and the implied volatility of the underlying asset

- The Black-Scholes model, Binomial model, and Monte Carlo simulation are methods for calculating the option premium

- Intrinsic value is the inherent value of an option based on the difference between the strike price and the current market price of the underlying asset

- Extrinsic value is the portion of the option premium that is not intrinsic value and represents the potential for the option to increase in value based on changes in market conditions or the passage of time

- Time decay is the decline in the value of an option as the expiration date approaches

- Implied volatility is a measure of the expected fluctuation in the price of the underlying asset

- Events such as earnings announcements or changes in market conditions can impact the option premium

- A decrease in the implied volatility of an options contract is known as a volatility crush

Definition of Option Premium

Options premium is the price of an options contract. It is determined by various factors, including the underlying stock price, the strike price, the expiration date, and the intrinsic and extrinsic value. The option premium is paid by the buyer to the seller when the options contract is purchased, and it represents the potential profit or loss of the trade depending on the future movement of the underlying stock. The option premium is one of the main factors determining whether the underlying trade will be profitable. Market makers factor in the expected move of the underlying asset into the option’s premium. This means that unless the option moves outside of the expected move, the buyer, or holder of the option, has a high probability of expiring worthless.

What is Option Premium?

Explanation of Premium As The Cost of an Options Contract

The option premium is the cost of an options contract. It represents the price that the buyer of the contract pays to the seller in exchange for the right, but not the obligation, to buy or sell the underlying asset at a predetermined price (the strike price) on or before a specified date (the expiration date). An option’s premium is a combination of intrinsic and extrinsic value. It derives its value from various factors, including the current market price of the underlying asset, the strike price, the expiration date, and the implied volatility of the underlying asset influence the option premium.

How Premium is Determined by Various Factors, Including Underlying Stock Price, Strike Price, Expiration Date, and Implied Volatility

Option premium is determined by various factors that can impact the perceived value of the options contract.

Some of the most important factors that influence premium include:

- Underlying stock price: The current market price of the underlying asset plays a significant role in the option premium. For call options, the premium will generally be higher when the underlying stock price is higher, as the option gives the buyer the right to buy the stock at a predetermined strike price. For put options, the premium will generally be higher when the underlying stock price is lower, as the option gives the buyer the right to sell the stock at a predetermined strike price.

- Strike price: The strike price, also known as the exercise price, is the price at which the underlying asset can be bought or sold if the option is exercised. The premium will be higher for options with a lower strike price, as the option gives the buyer the right to buy or sell the stock at a price below the current market price.

- Expiration date: The expiration date is the date on which the options contract expires. The premium will generally be higher for options with a longer expiration date, as the option potentially gives the buyer more time to profit from the trade.

- Implied volatility: Implied volatility measures the expected fluctuation in the underlying asset price. Options with higher implied volatility will generally have a higher option premium, as the options are perceived as having a greater potential for price movement.

How is Premium Calculated

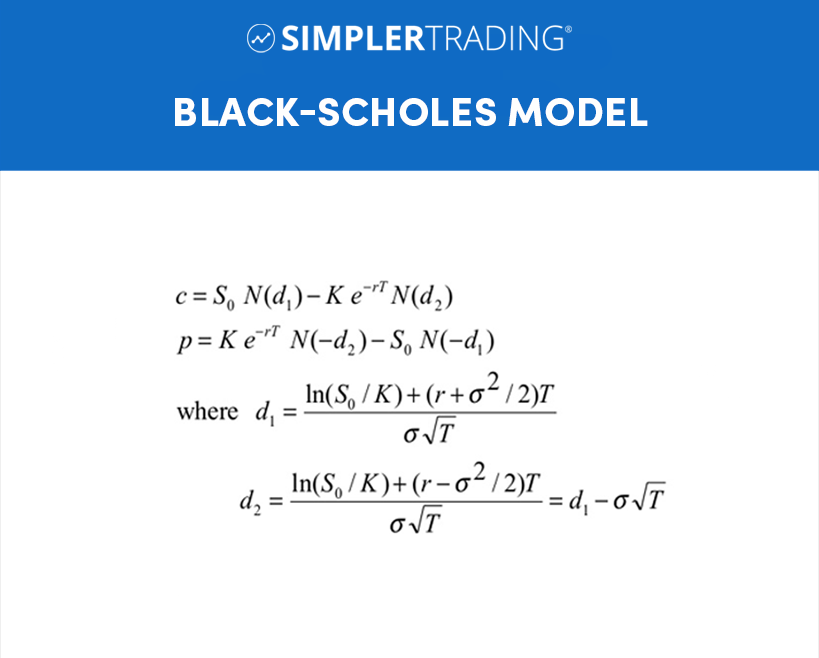

Explanation of the Black-Scholes Model for Calculating Option Premium

The Black-Scholes model is a way to calculate the fair price, or theoretical value, of an options contract based on certain assumptions. These assumptions include the current price of the underlying asset (the stock, for example), the strike price, the expiration date, the risk-free interest rate (the rate at which someone could lend or borrow money with no risk), and the implied volatility of the underlying asset (a measure of how much the price is expected to fluctuate).

To use the Black-Scholes model, you plug these variables into a specific formula, and the output is the option premium. The Black-Scholes model is a widely used and respected method for calculating option premiums, but it does have some limitations. For example, it only works for European-style options (options that can only be exercised at expiration). It doesn’t consider dividends or other real-world factors that can impact the option premium. As a result, other models like the Binomial model and Monte Carlo simulation have also been developed to provide more accurate option premium calculations in different situations.

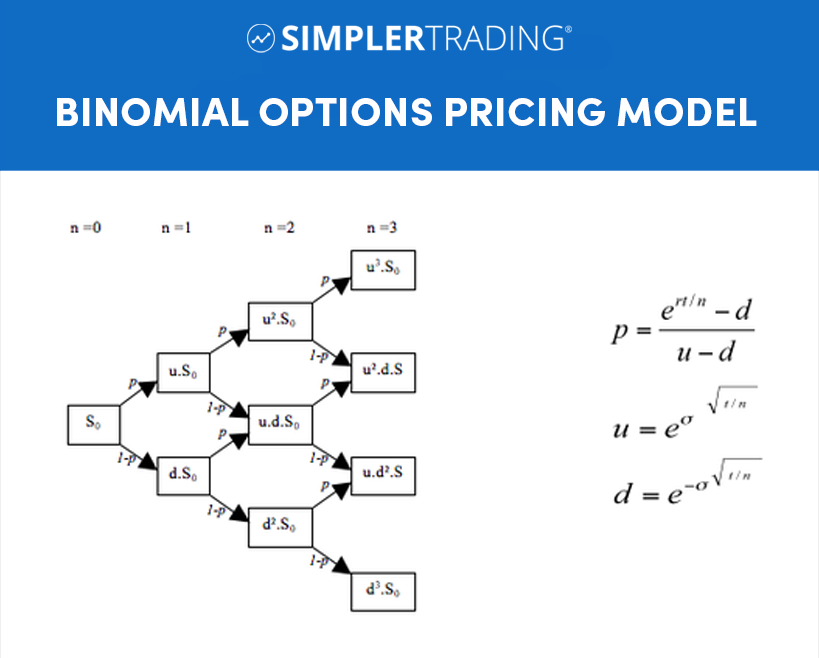

Binomial Options Pricing Model

The Binomial model is a method for pricing options that is based on the idea that the underlying asset’s price can only move in two possible directions: up or down. This contrasts the Black-Scholes model, which assumes that the underlying asset’s price follows a continuous trajectory.

To use the Binomial model, you first need to determine the two possible future prices of the underlying asset, called “up” and “down.” These prices are based on the underlying asset’s current price, the time until expiration and the underlying asset’s expected volatility. You then calculate the option premium for each of these possible future prices and the probabilities that they will occur. The option premium is the sum of these two calculations, weighted by the probabilities of each outcome.

The Binomial model is more flexible than the Black-Scholes model, as it can consider factors such as dividends and the ability to exercise the option before expiration. However, it can be more complex to use, as it requires the calculation of multiple potential future prices and probabilities.

Monte Carlo Simulation Pricing Options Premium

Monte Carlo simulation is a way to use a computer to estimate the price of an options contract by generating a large number of random outcomes for the underlying asset’s price. These simulated outcomes are based on certain assumptions about the underlying asset’s price movements, such as the expected volatility and the expected returns. The option premium is calculated as the average of these simulated outcomes, taking into account the probability of each outcome occurring.

Monte Carlo simulation is a useful tool for options pricing because it allows you to consider a wide range of potential future price movements for the underlying asset. However, it can be computationally intensive, requiring running the simulation many times to generate accurate results. As a result, it is often used with other pricing options methods, such as the Black-Scholes model or the Binomial model.

Intrinsic Value as a Factor in Options Premium

Intrinsic value is a key factor in the price of an options contract. It represents the inherent value of the option based on the difference between the strike price and the current market price of the underlying asset.

For example, consider a call option with a strike price of $50 and an underlying stock trading at $60. The option’s intrinsic value would be $10, as the option gives the buyer the right to buy the stock at a price ($50) lower than the current market price ($60). On the other hand, if the underlying stock were trading at $40, the intrinsic value of the option would be $0, as the option gives the buyer the right to buy the stock at a price ($50) that is higher than the current market price ($40).

Intrinsic value is an important consideration for options traders, as it represents the minimum value that an options contract could potentially have. When the intrinsic value is positive, the option has at least some inherent value based on the difference between the strike price and the current market price of the underlying asset. On the other hand, when the intrinsic value is zero or negative, the option has no inherent value and is considered “out of the money.”

Extrinsic Value as a Factor in Options Premium

Extrinsic value, also known as a time value or implied volatility, is a key factor in the price of an options contract. It represents the portion of the option premium that is not intrinsic value.

Intrinsic value is the inherent value of an options contract based on the difference between the strike price and the current market price of the underlying asset. Extrinsic value is the portion of the option premium that is not intrinsic. It represents the potential for the option to increase in value based on changes in market conditions or the passage of time.

For example, consider a call option with a strike price of $50, an underlying stock trading at $60, and an option premium of $12. The option’s intrinsic value would be $10 (the difference between the strike price and the underlying stock price), and the extrinsic value would be $2 (the option premium minus the intrinsic value). The option’s extrinsic value represents the potential for the option to increase in value based on changes in market conditions or the passage of time.

Extrinsic value is an important consideration for options traders, as it represents the potential for the option to increase in value beyond its intrinsic value. Factors that can impact the extrinsic value of an options contract include time decay, implied volatility, and changes in market conditions.

How Does Premium Change Over Time?

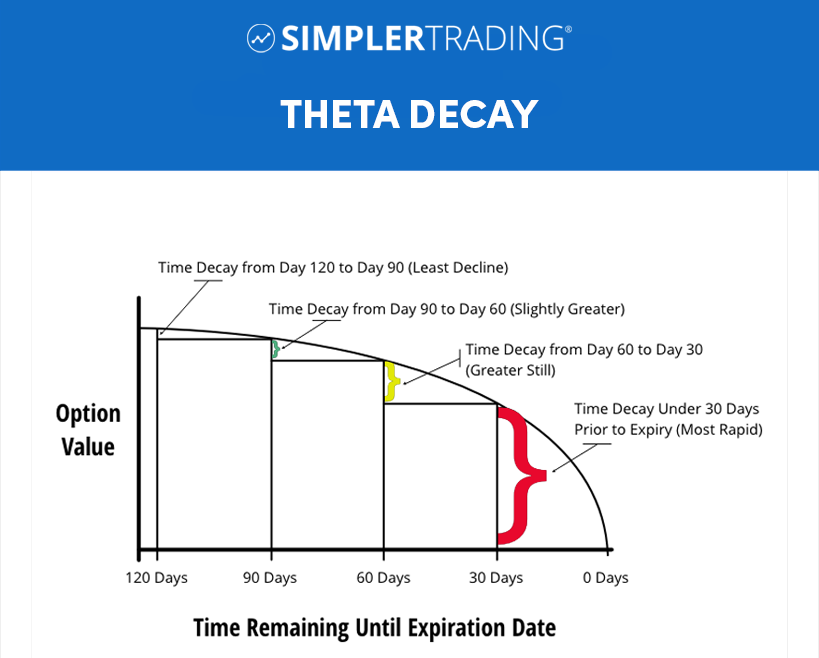

Time decay is the decline in the value of an options contract as the expiration date approaches. It is a key factor in the option premium and can significantly impact the potential profitability of an options trade.

As the expiration date of an options contract gets closer, the time remaining for the option to increase in value potentially decreases. This decrease in the potential for the option to increase in value is known as time decay. Time decay is generally more rapid in the final weeks before expiration, and it can significantly reduce the extrinsic value (also known as time value) of an options contract.

For example, consider a call option with a strike price of $50, an underlying stock trading at $60, and an option premium of $12. Suppose the option has three months until expiration. In that case, the extrinsic value (the portion of the option premium that is not intrinsic value) may be higher, as there is more time for the option to increase in value potentially. However, if the option only has one week until expiration, the extrinsic value will be lower, as there is less time for the option to increase in value potentially.

Time decay is an important consideration for options traders, as it can impact the potential profitability of a trade. For example, a trader who is long (buying) an option may see their potential profit decrease due to time decay, while a trader who is short (selling) an option may benefit from time decay.

The Relationship Between Premium and Implied Volatility

Implied volatility is a measure of the expected fluctuation in the underlying asset price. It is an important factor in the option premium and can significantly impact the price of an options contract.

Generally, options contracts with higher implied volatility will have a higher option premium, as the options are perceived as having a greater potential for price movement. On the other hand, option contracts with a lower implied volatility will have a lower option premium, as the options are perceived as having a lower potential for price movement.

For example, consider two call options with the same strike price and expiration date, but with different underlying stocks. Suppose one underlying stock has higher implied volatility (meaning it is expected to fluctuate more in price). In that case, the call option on that stock will have a higher option premium than the call option on the stock with lower implied volatility.

Understanding the relationship between the option premium and implied volatility is important for options traders. It can help them decide which options to buy or sell and at what price.

How Events Such as Earnings Announcements or Changes in Market Conditions Can Impact Premiums

Events such as earnings announcements or changes in market conditions can significantly impact the option premium. These events can alter the option contract’s perceived value, resulting in changes to the option premium.

For example, consider a call option with a strike price of $50 and an underlying stock that is expected to release earnings in the near future. If the earnings report is expected to be strong, the premium may increase, as the options are perceived as having a greater potential for price movement.

Similarly, changes in market conditions can also impact the premium. For example, suppose the overall stock market is experiencing a period of high volatility. In that case, options on stocks in that market may have a higher option premium, as they are perceived as having a greater potential for price movement. On the other hand, if the market is experiencing a period of low volatility, options on stocks in that market may have a lower option premium, as they are perceived as having a lower potential for price movement.

Understanding how events and changes in market conditions can impact the premium is important for options traders, as it can help them make informed decisions about which options to buy or sell and at what price.

Volatility Crush and Options Premium

Volatility crush refers to a decrease in the implied volatility of an options contract. It is a phenomenon that can occur after a significant event, such as an earnings announcement or a change in market conditions.

When the implied volatility of an options contract decreases, it can result in a decrease in the option premium. This is because the options are perceived as having a lower potential for price movement and, therefore, are less valuable. The decrease in the option premium is often referred to as a “crush,” hence the term “volatility crush.”

Volatility crush can have significant implications for options traders, as it can impact the potential profitability of a trade. For example, a trader who is long (buying) an option may see their potential profit decrease due to a volatility crush. In contrast, a trader who is short (selling) an option may benefit from a volatility crush.

Understanding the potential for volatility crush and how it can impact the premium is an important consideration for any options trader.

Conclusion

In conclusion, understanding the basics of option premiums is essential for any trader looking to enter the world of options trading. By considering factors such as the underlying stock price, strike price, expiration date, and implied volatility, traders can make informed decisions about which options to buy or sell and at what price. Methods such as the Black-Scholes model, Binomial model, and Monte Carlo simulation can be helpful tools for calculating the option premium. Understanding concepts such as intrinsic value, extrinsic value, and time decay can help traders understand an options trade’s potential risks and rewards.

If you’re interested in learning more about options trading and getting the opportunity to hear from and interact with professional traders with decades of experience, consider signing up for the $7 trial to the Simpler Central live trading room. In this room, traders conduct thorough technical analysis of stocks and make real trades with real money. It’s an excellent opportunity to learn from the pros and improve your own options trading skills. Don’t miss out – sign up today!

There are several methods that can be used to calculate the option premium, including the Black-Scholes model, the Binomial model, and Monte Carlo simulation. These methods take into account factors such as the current price of the underlying asset, the strike price, the time to expiration, the risk-free interest rate, and the expected volatility of the underlying asset.

Intrinsic value is the inherent value of an options contract based on the difference between the strike price and the current market price of the underlying asset. For example, if the strike price of a call option is $50 and the underlying stock is trading at $60, the intrinsic value of the option would be $10 (the difference between the strike price and the underlying stock price).

Extrinsic value, also known as time value or implied volatility, is the portion of the option premium that is not intrinsic value. It represents the potential for the option to increase in value based on changes in market conditions or the passage of time.

Time decay is the decline in the value of an options contract as the expiration date approaches. It is a key factor in the option premium and can have a significant impact on the potential profitability of an options trade.

Implied volatility is a measure of the expected fluctuation in the price of the underlying asset. It is an important factor in the option premium and can significantly