It’s difficult to watch an evening program on the networks without viewing commercials featuring anxious retirees mulling over their retirement accounts with a cup of coffee. Many of these commercials feature retired couples walking their dog, window shopping, or riding their cruiser bikes along the boardwalk. Where are the real people who get stuck in traffic after dropping toddlers off at daycare all week? Where are the single moms and dads trying to make ends meet? Of course, they have dreams for retirement, too!

Let’s be honest for a moment. The pictured grandparents have already made the major decisions regarding their income. They saved and put back money when employees still had pension plans, and social security was a guarantee. Even the tiny amounts they put back still had time, years even, to grow. Employees today often don’t have the same luxuries. This makes taking responsibility for retirement income essential.

Financial Literacy Tips that Work

The rising living and housing costs mean that savings accounts and income-based investing won’t provide enough funds when they retire to live as comfortably as they were employed with (hopefully) good insurance and tax deductions. Putting back cash now to have the necessities 30, 40, or 50 years down the road is what everyone should consider.

As an essential part of your life journey, it’s worth evaluating your progress for retirement savings once per year. When they gather together their tax portfolio, many people find that each spring is a great time to put together a list of retirement savings and the investment portfolios in the accounts.

Do you Need Help Picking Stocks for Retirement?

For some traders and investors, retirement may not be for a while, for others, it may be around the corner. But, that doesn’t mean you shouldn’t go without any guidance or mentorship when building your portfolio. However, that’s where The MEM Edge can help. The MEM Edge is personally operated by Mary Ellen Mcgonagle, who has over 20 years of experience picking some of the best stocks in the market. Sign up today and get her report twice a week on high-quality stocks in the market.

Video Guide to Growing Your Retirement Portfolio

How to Plan for My Retirement?

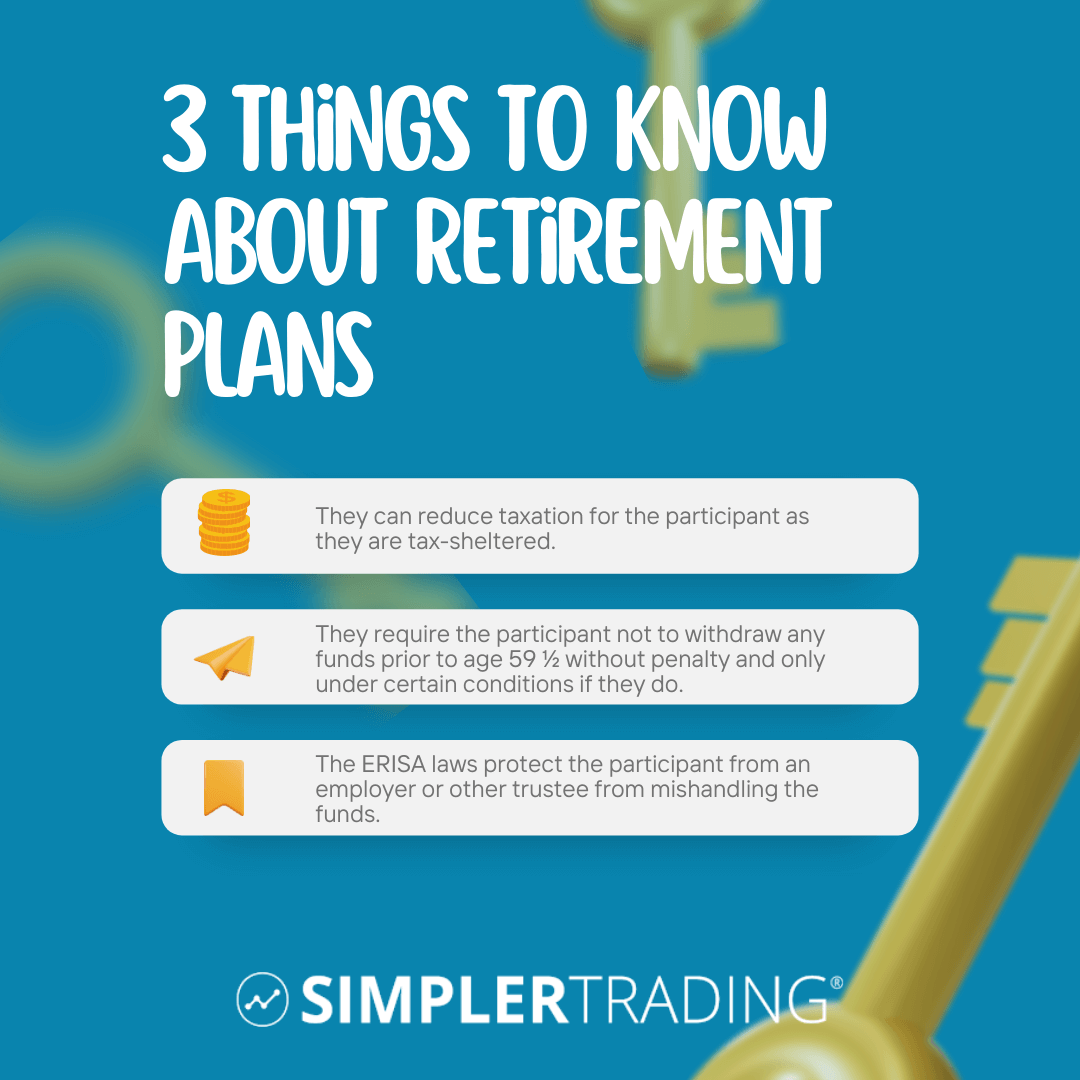

Many people never actually ponder this question until their employer hands them 401(k) paperwork. Those self-employed will often take more time to contribute until their business grows enough to pay them a salary. The unique benefits they offer are the most important thing to understand about retirement plans such as the 401(k), 403(b), and IRA.

- They can reduce taxation for the participant as they are tax-sheltered

- They require the participant not to withdraw any funds before age 59 ½ without penalty and only under certain conditions if they do

- Further, the ERISA laws protect the participant from an employer or other trustee from mishandling the funds

The Basics of IRAs

There are many compliance laws and regulations for banks and trustees for IRA funds to follow. However, for the individual, all that is required is to go to their bank or brokerage firm and open an IRA account. Often, IRA accounts can be opened online, and professionals will see to it that they are appropriately invested. But, let’s go over the basics of IRAs, Roth IRAs, SEP, and Simple IRAs. Individual Retirement Accounts are designed to allow individuals to have access to retirement vehicles (yes, that’s really a thing) that would enable their money to grow without tax consequences until a later date.

IRAs allow individuals to invest in stocks, bonds, mutual funds, and ETFs with their contributions. IRAs purchased at banks often allow participants to buy Time Deposits or other low-risk investments. Investors should ask what investment options are available before investing or opening an account. When individuals use a brokerage account, they can elect to have a self-directed investment portfolio or have the broker select the investments for a fee.

Persons who have an employer who does not offer a 401(k) account or have reached their maximum contributions may also invest in a traditional IRA. The maximum contribution to IRAs is adjusted from time to time, but currently, individuals can contribute up to $6,000 in 2022. The contribution max for an IRA will increase to $7,000 for persons age 50 or older. Having the ability to allow investment gains to grow tax-deferred enables them to increase the growth rate significantly. In certain circumstances, IRA contributions may be tax-deductible. It’s essential to notify your tax advisor if you make contributions each year.

Roth IRA contributions are made with after-tax dollars for even more investment power. After-tax contributions will affect the taxes paid when distributions are made later. But it does not affect the capital gains tax within the account. Since Roth contributions are made with after-tax dollars, if individuals meet requirements, they don’t pay taxes when they take money out after retirement age. Retirees will be in a lower tax bracket; therefore, they will enjoy more tax benefits.

Interestingly, Roth 401(k) contributions are sometimes available in employer plans. If so, individuals who do not need the tax benefits of lowering their taxable income now can benefit significantly by contributing post-tax dollars for retirement. A visit with a tax professional to determine your tax bracket can decide if this step makes the most sense. SIMPLE and SEP IRAs are only available to business owners who want to contribute their employee accounts. The rules and regulations are detailed and are designed to offer similar benefits to a 401(k).

Self-Managed Retirement Accounts

It’s important to note that the bulk of retirement accounts should be invested judiciously regardless of their retirement vehicle. day and swing trading accounts should be maintained separately from the primary money you plan to invest for retirement. Investors should open a separate account just for self-managed trading purposes that will not be critical for essentials later.

Specific IRA and 401(k) plans allow individuals to manage their own investments. If this is your intention, you will need to look specifically for a firm that will enable you. So that way, you can focus on exchange-traded funds (ETFs), mutual funds, options, time deposits, or highly aggressive stocks – the brokerage firm needs to know before opening the account so that they may meet your needs.

How much should I contribute?

Many people look at their debts – mortgage, car, credit cards – as if these are valid reasons not to contribute to retirement. They are not. Debts should be temporary. If debts and spending are out of control, this could be an excellent time to consider whether changes need to be made in the household budget. When 401(k) plans were first introduced, many employees were limited to how much they could contribute to their retirement plans by the ERISA laws. However, those laws have been revised, and employees have much more flexibility in the amount they can contribute.

The simple answer to how much you should contribute? Without even considering whether or not you can contribute, find out if the employer has a contribution match. If nothing else – do that. Even better, double it. There will never be a better time than now. The question to ask is, based on the inflation rates and the lifestyle you plan to have, how much monthly or annual income will you need, and for how many years.

If momma plans to travel to every continent and dance in the conga line after she’s free from the nine-to-five, she can draw out a plan to make that happen. Some people assume that having $500,000 as they reach retirement age will suffice. But, this number is easily underestimated, even for frugal senior citizens.

One reason, specifically, is healthcare and medical spending. These are both big-ticket items that early-career individuals usually will not have. It’s good to remember that it will be a good place to be when you have positioned your finances accordingly. Then, maybe you can audition to be in those cheeky commercials – or possibly commercials that feature retirees who are skydiving. However, if you need help positioning your retirement portfolio, you should consider signing up for the The MEM Edge. By signing up today you will gain access to buy and sell stock candidate each week, critical market updates, and actionable stock ideas and insights on the broader market.

FAQs on Retirement Savings

A: Most often, IRA and other retirement vehicles contain mutual funds – as opposed to exchange-traded funds and stocks for investing. The most simple reason for this is that mutual funds have fund managers who oversee the funds on a daily basis. Mutual funds are not designed to be easily bought and sold. However, just like cars, these accounts can vary and offer different “packages” to the consumer. This makes it important for the individual to establish an account protocol for money management regarding monies that are strictly earmarked for retirement only. The money you’re willing to lose should be maintained separately from the money you need for retirement.

A: Covered calls offer a relatively low-risk alternative to increase investment returns. Investors may consider writing covered calls on the stock they have in their IRAs if their account allows it. Traders should ask their broker or brokerage firm prior to opening an account. This approach to trading options has the potential to produce returns on investment, regardless of whether the stock price rises or falls, when executed properly. On the other hand, it can also limit the potential returns on the upside should the stock price continue to rise.

A: In a nutshell, yes you can – but with limited strategies and only if the account is opened properly. Options are risky and aren’t appropriate for everyone. You can’t borrow money from an IRA and this limits strategies to buying puts and covered calls. Options traders aren’t able to sell shorts, naked options, or borrow on a margin account.

A: According to the IRS and generally speaking, you will have to withdraw from regular IRAs, SEP IRAs, Simple IRAs, and other retirement accounts when the account holder reaches the age of 72. However, for Roth IRAs withdrawals are not required by the owner until they are deceased.

A: Absolutely; however, you may have to do it quickly so you don’t get penalized. If you are interested in doing that, first speak to your brokerage firm where the IRA is established and your employer to figure out what necessary steps need to be taken.