About – VWap Max

The VWAPMax End of Day Indicator originally released with the Sub Market Sonar class indicators. – ST_VProfile – ST_VScore – ST_VWAP

What is the VWap Max?

ST_VWAPMax_EndOfDay

ST_VWAPMax_Intraday

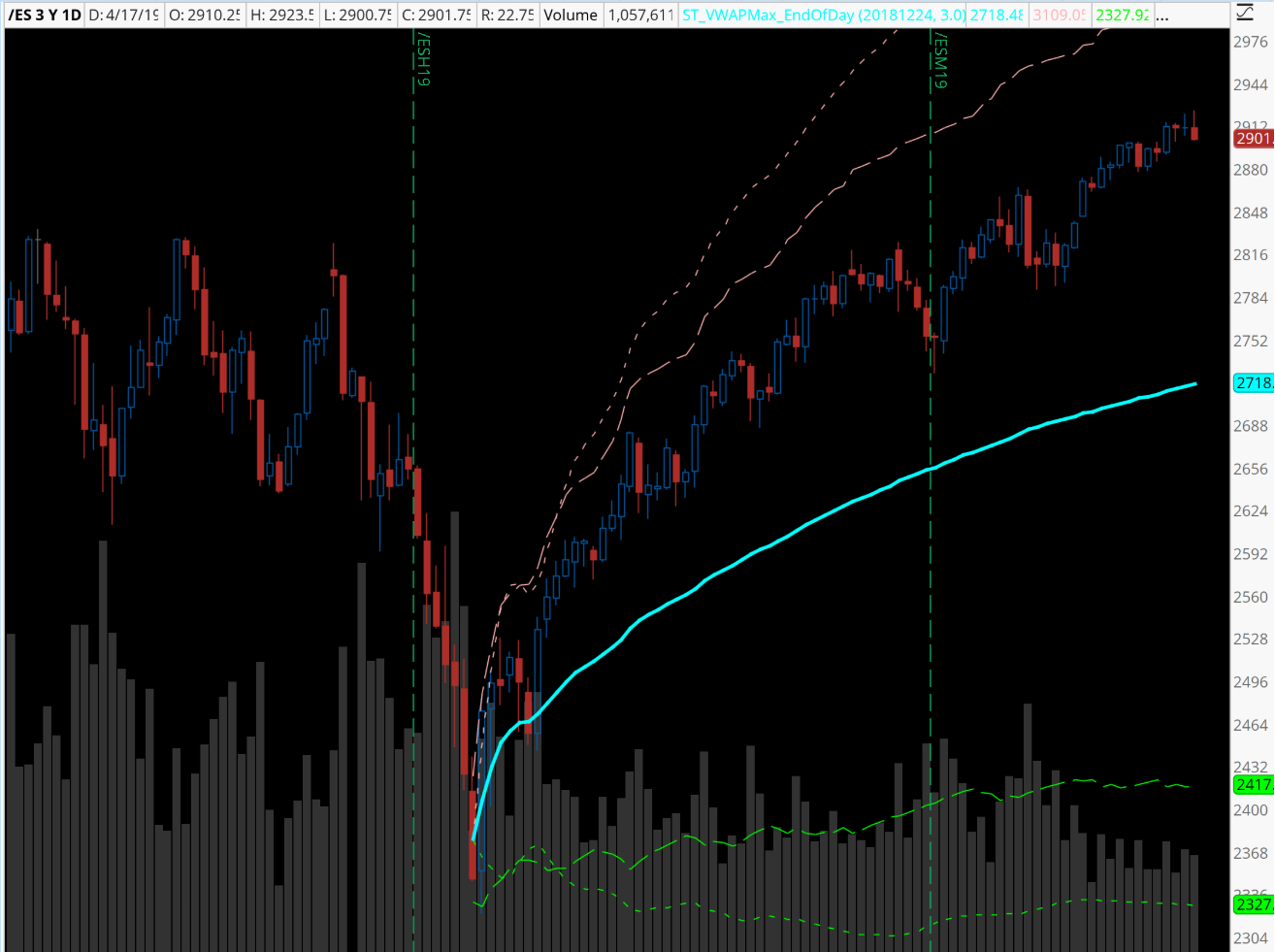

The core of the VWAPMax indicator is the display of the volume weighted average price. We often use moving averages on a chart which are constructed by simply averaging the price over a certain number of bars. The volume weighted average price takes this idea a step further by weighting each bar’s price by the volume traded during that bar. Mathematics aside, the VWAP is designed to show at a glance the average price level of participants involved in the market selling since the anchor point of the VWAP. Heavier volume at certain price points drags the VWAP closer to that price whereas light volume trading has far less “pull.”

Additionally, the VWAPMax indicator displays an envelope around the VWAP which represents the theoretical maximum permissible deviation away from the VWAP.

There are two versions of the VWAPMax. One is designed for daily charts and may be anchored to any date present on the chart (i.e. there must be a bar on the chart corresponding to the date you choose). This is the VWAPMax End of Day tool. The second version is designed for use on Intraday charts and may be anchored to any time present on the chart. This is the VWAPMax Intraday tool.